Do Not Let the Laggards Write the Story

Why selection bias is warping our view of India’s consumption growth

I’ve been talking about this for a while now and yet, the steady stream of “slowdown” headlines refuses to die down. Every few days, someone points to a weak data point from one company or category and builds a grand narrative around it. But if you zoom out and look closely, the picture is far more nuanced and in many cases, the opposite of what the headlines suggest.

The Anecdote Trap

How can it be that on one end HUL says it may not sell enough this quarter and till October, while Blinkit continues to grow at 100%+?

How can it be that box office theatres are barely running on single-digit occupancy, but concert tickets by global headliners are getting sold out before you can even get your hands on them?

How can it be that apparel retail among the bigger brands is growing at high single to low double digits, but value retailers are exploding with high double-digit growth?

These are not contradictory facts. They are signs of a diverging growth cycle, where traditional leaders no longer fully represent the behaviour of the market.

Selection Bias in Action

This is a classic case of selection bias, where a handful of familiar names become the proxy for the entire sector, and anchoring bias, where we stick to outdated indicators to assess a new reality.

For the longest time, we looked at HUL as the bellwether for FMCG, PVR for entertainment spends, and Trent for apparel retail. But the consumption basket has expanded.

Customers have 200× more options than they did a decade ago.

Distribution lives inside their house, thanks to 10-minute delivery.

The plethora of brands across price points, niches, and channels is unprecedented.

The dopamine hits are no longer limited to likes and comments on social media or matches on dating apps, they now extend to fulfilment speeds in commerce.

Look Deeper, Flip the Narrative

The reality is: if you look closely and look deeper, a sector that seems stagnant because its old leaders are slowing may actually be in the middle of a new inflection. The names leading the next wave of growth might be ones you’ve never heard of.

Long story short, there is no broad slowdown. What we’re witnessing are the perils of anecdotal data in a rapidly diverging growth cycle.

Closing Thought

Markets evolve. Consumers evolve faster. Anchoring on legacy leaders to read a new consumption cycle is like checking the wind direction by staring at last season’s weather report. Don’t let the laggards write the story.

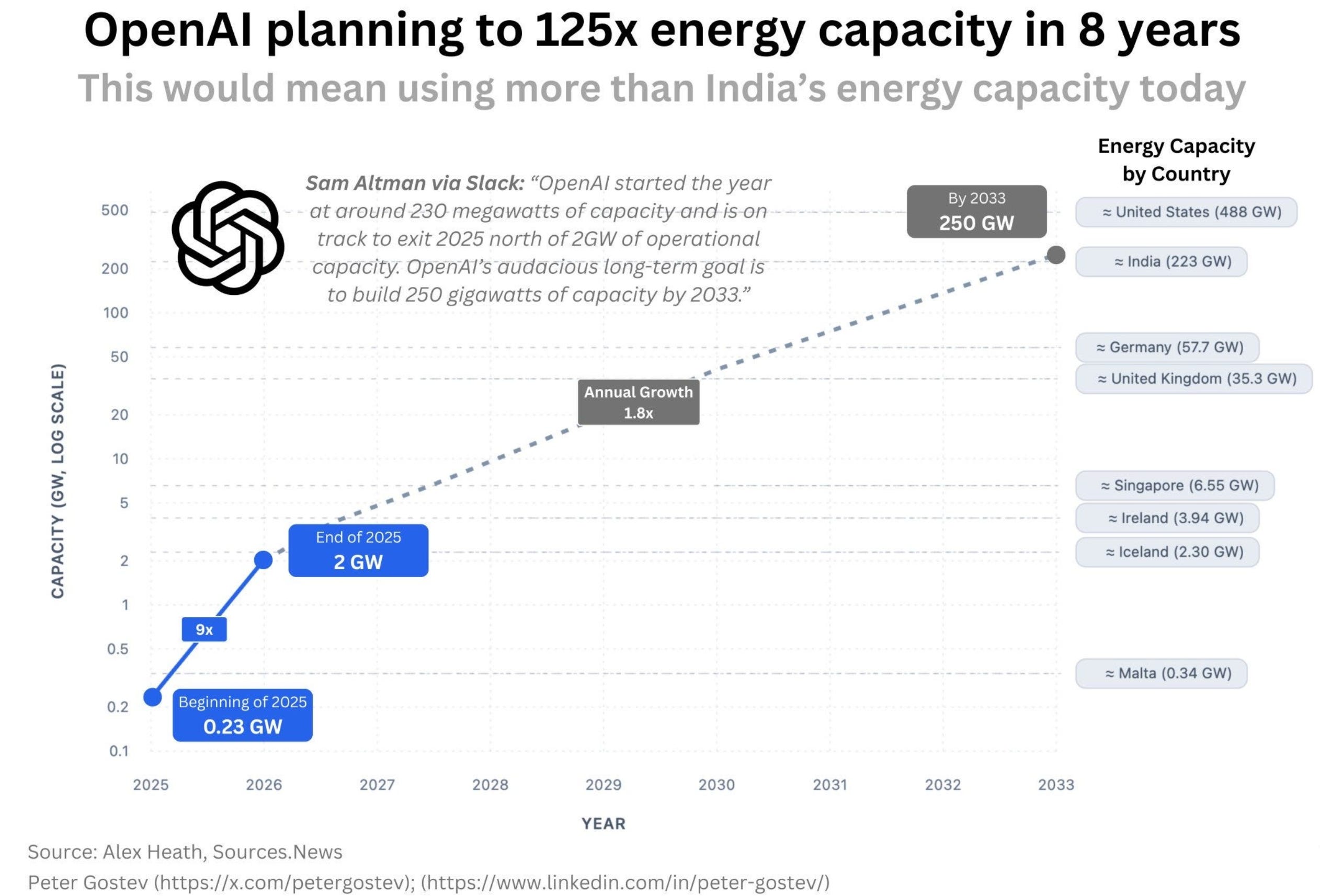

Is Power the new AI play?

You may have seen this image doing the rounds for a while. In the entire AI value chain, people talk about semi conductors, fab, data centres, servers - but guess what is going to power all of it?

Energy!

This is where the next war is already underway - everyone wants energy security - no one wants to be dependant on anyone because the new wars are also getting fought on energy - critical minerals were already there in the list of prizes that were up for grabs.

We are currently preparing our 3rd Webinar for this year for the Beta to Alpha series, and slowly we will be sharing more details about the webinar with you.

Where are we preparing for this month’s detailed deep dive?

We have got multiple requests to break down the AI value chain. While globally it has become very clear, USA and China are taking away a bulk of the capital flows, there is a massive value chain that is all encompassing.

While the India growth story is not over, there is clearly new found appetite and interest to be participants in this space - from the policy push to new capital finding application to setting up fab units or using a SAAS model for renting compute power.

In case you are interested to attend this session, click below ⬇️

sometimes i feel the biggest filter is demand & supply and competition intensity in a category. Once competition intensity increases, best to be cautious as an investor. HLL's biggest

moat was it's distribution & sales, now with D2C and QC that is getting blunted. Add to it the smaller players are coming out with better products, this coupled with with a more democratized media is really hurting big guys. Remember big guys have big cost structures and are are slow to move, add to it profitability pressures - so might be cut corners on product . HLL's product plays are in all mature categories so more competition with better products. I fell FMCG will go the European way with smaller brands gaining strength in pockets but this small nibbling by small brands will add up for the big guys

Interesting.