Every Rupee Needs a Purpose, a Timeline, and an Instrument 🧭

Bond yields crossed 7%. A Rs 2 crore short-term debt fund parking ended in a loss. Here is the yield curve risk most retail investors never see coming.

There is a version of investing most people never talk about.

Not equities. Not that stock that tripled. Not the next multi-bagger.

Debt.

Specifically, how you allocate to debt. And within that, how you park short-term money with precision.

When I headed treasury for a large hotel chain, my mandate was simple and non-negotiable: liquid funds and fixed deposits. No duration calls. No yield curve plays. No high-risk credit paper.

The objective was never to maximise absolute return. It was to optimise risk-adjusted return within a tight liquidity framework. You needed the money when you needed it. You could not afford a mark-to-market surprise on day one of a quarter.

That discipline, I have come to realise, is severely under-appreciated in retail investing conversations.

The Case Study

A few days ago Beta to Alpha quietly announced it is entering the transaction side of mutual fund investing. We are starting with the basics, building the pipeline right, and learning alongside you.

And almost immediately, an interesting case landed on our desk.

Someone came to us with Rs 2 crore that needed to be parked for short-term needs. The intent was straightforward: deploy the capital, earn some yield, redeem when required.

Actual allocation: 50% in an ultra-short duration fund, 50% in a low duration fund, across two AMCs.

Forty days later, when the redemption request came in, one of the funds showed a loss.

Let that sit for a moment.

A debt fund. Designed for safety. Used for short-term parking. Showing a loss.

What Went Wrong

The mechanics are not complex once you see them clearly.

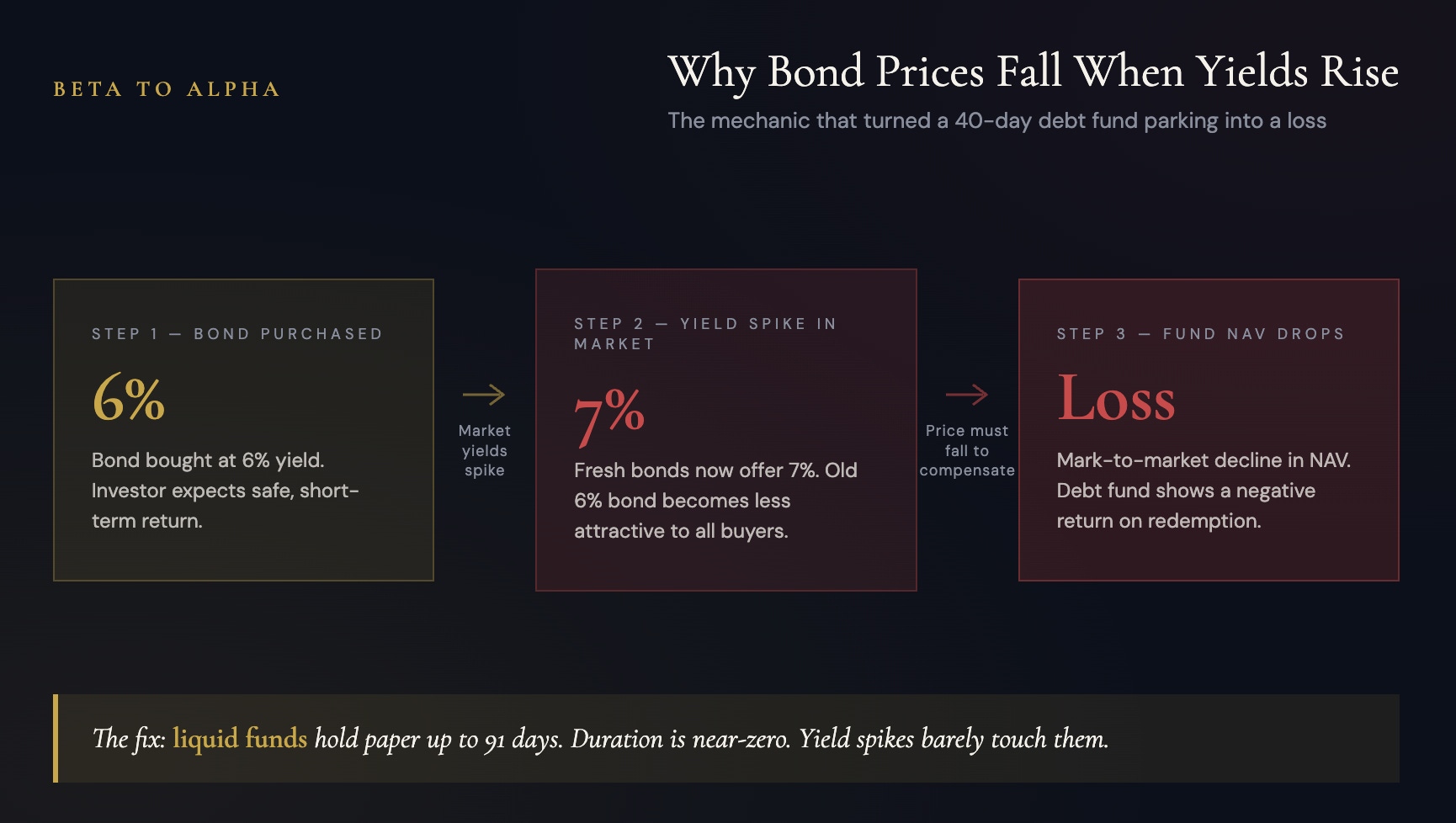

During that 40-day window, bond yields in India crossed the 7% mark.

Plain-language cause and effect: if a bond was purchased yielding 6%, and market yields have now moved to 7%, that older bond becomes less attractive. No one wants to hold a 6% bond when fresh paper is offering 7%. So the price of the older bond falls to equalise.

In a mutual fund, this price decline shows up as a mark-to-market loss on the NAV.

Ultra-short duration and low duration funds carry slightly longer maturity profiles than liquid funds. That means they carry more duration risk. When yields spike, the price impact is proportionally larger.

The investor never changed her intent. She never wanted to take a duration call. She wanted safe, short-term parking with marginally better yield.

But the fund category she chose carried duration risk that was fundamentally mismatched with her actual purpose.

The Fix

A simple liquid fund would have been the right instrument.

Liquid funds hold paper with maturities up to 91 days. Duration is ultra-short. Yield curve risk is minimal to negligible.

Yes, the return would have been 5 to 6% instead of a potential 6 to 7%.

But there would have been zero exposure to a mark-to-market loss on a 40-day horizon.

The purpose of the money defines the instrument. Not the other way around.

Chasing an extra 50 to 100 basis points without understanding the risk profile of the underlying portfolio is not conservative investing. It is speculation wearing a conservative label.

The Broader Lesson

In equity investing, we obsess over entry points, sectors, valuations, and earnings cycles.

In debt, most retail investors do not think at all. They either park in a fixed deposit, or they ask their distributor for something that gives slightly better than FD returns.

That second category is where most of the mistakes happen.

The yield is not the only variable. Duration is a risk. Credit quality is a risk. Liquidity is a risk. And the alignment between your time horizon and the fund’s underlying maturity profile is the most important variable of all.

When I ran treasury, every rupee had a purpose, a timeline, and an instrument matched to it precisely. That framework applies equally, perhaps more urgently, to retail investors managing their own debt allocation.

Do not let marginal yield chase overwrite the clarity of purpose.

What We Are Building

At Beta to Alpha, we are building a framework for debt investing that begins with first principles.

Purpose of capital. Time horizon. Yield requirement. Risk tolerance. And only then, instrument selection.

If you need help reviewing your mutual fund allocation, reply with “Interested” and we will take it forward.

More than 119+ readers have now attended Growth Titans of Q3. As we gear up for Growth Titans of Q4, this is a great time to catch-up on our last quarterly check-in.

Request recording access below.

Disclaimer: Neither Saket Mehrotra nor Beta to Alpha is a SEBI registered investment advisor. Views are my own and do not represent my previous or current employer. Any mention of stocks and securities is not a recommendation to buy / sell. The author may hold positions in the stocks mentioned and sell it without prior notice. Please do your own due diligence before investing. The purpose of this newsletter is for educational purposes only.