Winter Stock in Summer

The Nifty Small-cap 100 has corrected 25% from its peak. Aggregate PAT grew 14% last year. The shopkeeper is ready to sell you a cashmere sweater at Rs 85. Nobody wants it.

Imagine walking into a store in June, asking for a winter sweater. The shopkeeper doesn’t put it on the front rack. He takes you to the back of the warehouse, digs it out from a pile, and offers it to you at Rs 100 against an MRP of Rs 399.

You push back. You say: how about Rs 85?

Notice what just happened. You are not asking about the quality of the cashmere. You are not asking if the design came from Paris Fashion Week. You are not asking about the sourcing, the GSM, or the brand. The only axis of debate is price. And even at a 75% discount to MRP, the buyer wants more.

That is the market for Indian small-caps today.

Before we delve deeper, I'm covering multiple macro insights and an evaluation of the current market scenario on March 15th alongside Growth Titans of Q3.

If you've been on the fence, this is your signal.

The Divergence That Matters

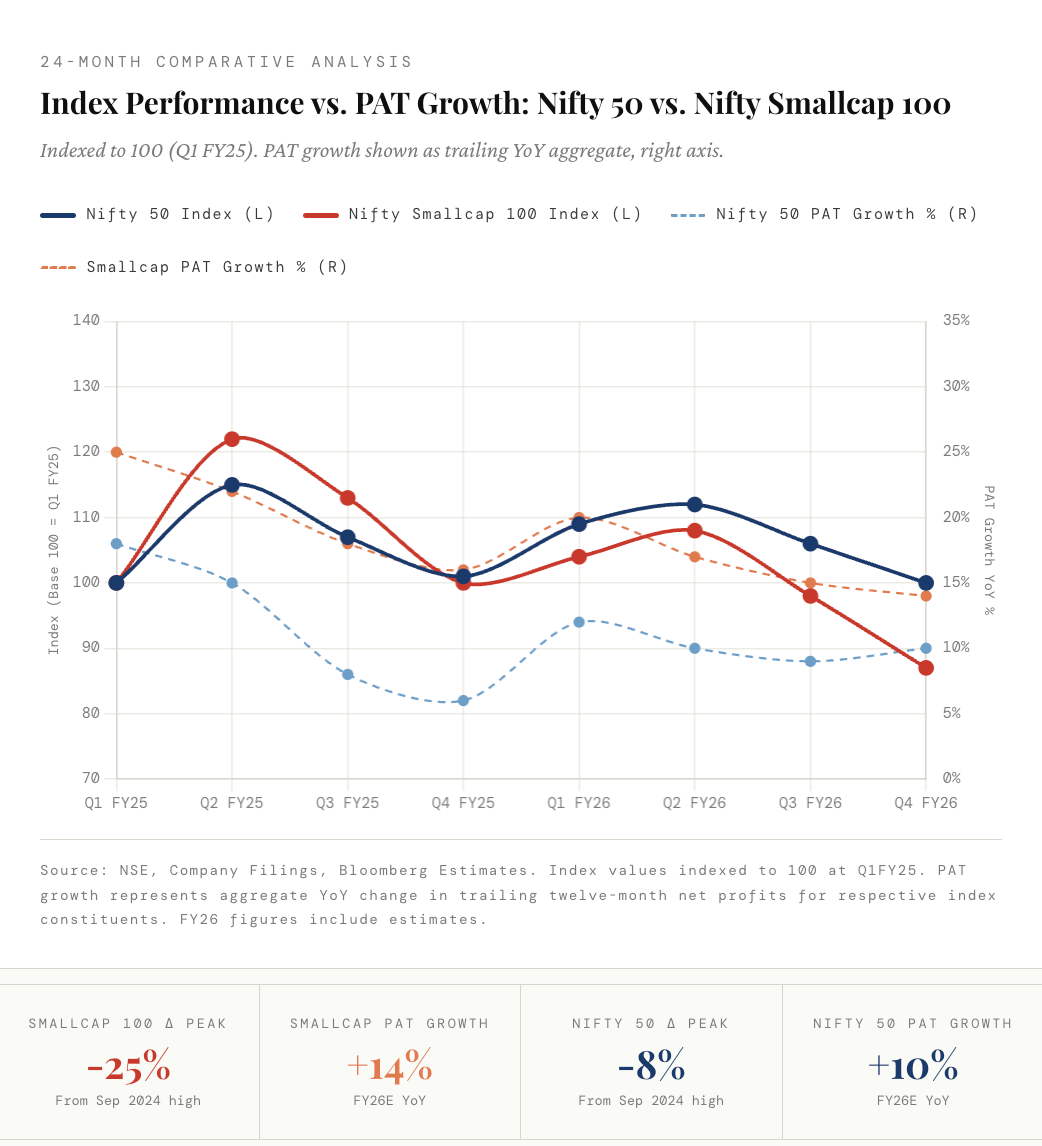

Look at the chart above. The Nifty Small-cap 100 is down approximately 25% from its September 2024 peak. The aggregate PAT of its constituent companies grew roughly 14% over the same period. Let that gap sit with you for a moment.

Prices fell. Profits rose. In any rational framework, that is a compression of multiples, not a compression of business quality. The market is not saying these companies are earning less. It is saying it does not want to pay for what they are earning. That is a sentiment statement, not a fundamental one.

The Nifty 50 tells a different story. Large caps corrected roughly 8% from peak, with PAT growth tracking at approximately 10%. The valuation discount between the two universes has rarely been this wide outside of a genuine earnings recession. We are not in one.

Why Nobody Wants the Sweater

Three forces are conspiring to keep retail and institutional money out of smallcaps right now. First, the memory of the 2021 to 2022 smallcap bubble is still fresh. Burned once, investors are wiring the current correction as a repeat rather than a reset. Second, liquidity in small-caps dries up faster in risk-off environments, and the global backdrop since late 2024 has been selectively risk-off. Third, fund manager career risk is real: no one gets fired for holding Reliance. Everyone gets questioned for holding a mid-sized auto ancillary at 22x earnings.

These are behavioural forces. They are not permanent. They are, in fact, precisely the conditions under which future returns are manufactured.

What History Says About the Warehouse

Every significant small-cap re-rating in India followed a period of exactly this: prices disconnected from earnings, sentiment uniformly negative, liquidity thin, and the dominant narrative asking why you would own something that “nobody wants.” The 2014 to 2017 run. The 2020 post-COVID reversal. Each time, the setup was a warehouse sale in summer.

The re-rating does not require a catalyst. It requires exhaustion. It requires the last seller to have sold. When that happens, even a modest uptick in risk appetite sends these names sharply higher because liquidity is thin on both sides.

The Framework That Guides Us

At Beta to Alpha, our Profit Pool Disruptors framework has always pointed to one simple truth: earnings inflection before market consensus is where the risk-adjusted return lives. Smallcaps today are not inflecting. They are holding. Earnings are growing at 14%. The market just refuses to price that growth.

That refusal is not permanent. But it will test your patience before it rewards your conviction.

The shopkeeper is in the warehouse. The sweater is Rs 85. The question worth sitting with is not whether it is cheap enough. The question is whether you know what you are buying, and whether you will still hold it when February arrives and everyone suddenly wants what you have been carrying since June.